3-D PRINTED TITANIUM IMPLANTS THAT PARTICIPATE IN THE HEALING PROCESS

Porous surfaces

In orthopedic implants it is common to create porous surfaces designed to promote ‘osseointegration’ – where a patient’s bone is encouraged to fuse with the metal implant to secure it firmly in place. The implant’s surface is covered with a carefully designed layer of lattice, which has the optimum spacing and strut thickness to enable living bone to grow into it and form a strong, load-bearing bond with the metal device.

Image above – SEM image of the porous surface of an acetabular cup.

So lattices have a number of attractive qualities, although their complexity and delicacy can make them challenging both to design and to manufacture.

Lattice design

Most lattice materials are made up of arrays of slender members that resemble familiar lightweight super-structures such as bridges and building frames, but obviously on a much smaller scale. These complex meso-structures can be produced additively in length scales that vary from microns to millimetres.

Image above – Cubic lattices with various length scales. The minimum producible scale is limited by the smallest strut thickness that can be manufactured on an additive machine, which can be as little as 140 microns on a laser powder-bed fusion machine with a 70 micron laser spot size.

Lattice structures can be regular (such as the cubic lattices shown above) or irregular, and designed to provide either homogeneous or heterogeneous properties. The length scale can vary throughout the lattice volume to tailor its properties – particularly its density and stiffness – in different locations.

Image above – Sectioned femur in which the internal trabeculae form an elegant three-dimensional latticework that mimics the structures seen in natural bones. The length scale and strut thickness vary throughout the lattice volume.

Lattice types

The choice of lattice geometry is critical to effective light-weighting, enabling porous materials that approach the strength of their solid counterparts, yet at far lower densities. Some porous structures such as foams are light, but not all that strong. Their structures are said to be ‘bending-dominated’, so that loads applied to the macro-structure are resisted by bending of the struts in the meso-structure. This makes them compliant and good for energy absorption.

By contrast, lattices that are ‘stretch-dominated’ carry their loads axially along the struts, either in tension or compression. Such structures are characterized by high levels of node connectivity, providing cross-bracing to prevent relative motion of the nodes. These ‘space frame’ meso-structures, like their large-scale architectural equivalents, provide the best strength-to-weight ratio.

Image above – The bending-dominated structure (on the left) is much weaker than the stretch-dominated structure (on the right).

Gyroids

Not all lattice materials comprise simple strut-and-node arrangements. Gyroids are triply periodic structures, built up of small cells of curved ‘minimal’ surfaces that repeat in all directions to form a regular structure. In certain circumstances, these structures can have higher specific strengths than regular diamond lattices. Image from Wikipedia.

Image above – gyroid lattice structures.

Architectured materials

Thanks to the flexibility of additive manufacturing, we can now design and build ‘architectured materials’ in which the meso-structure has been tailored to provide specific mechanical properties.

Image above – Architectured material with heterogeneous properties. Its fibrous structure exhibits, like a composite, different stiffness in different directions.

Hybrid lattice structures

As we have seen above, lattices can be integrated neatly into product designs. They can also be combined with other weight-saving techniques such as topological optimization. The super-structure of the part can be shaped using generative design, with further weight-saving gains achieved by applying a lattice meso-structure onto some of the super-structure.

Image above – An architectural ‘spider’ bracket from titanium combines topological optimization with lattice materials to minimize component mass. ww.youtube.com/watch?v=WMCR6VBSV-E

Image above – cross-section of the spider bracket showing the combination of solid and lattice structures.

Lattice build preparation

A key computational challenge for the additive manufacturing of lattices is how these complex structures are represented and converted into a build file. Most additive components are designed in 3D CAD and then converted into a triangulated surface format (STL). These STL models are then sliced into thin layers from which we compute the laser paths needed to build up the part.

If we take this approach with lattices, especially those with a small length scale, then we quickly run into enormous models and interminable build file preparation. Specialists in lattice design and additive manufacture are looking at ways to simplify the generation and manufacture of such complex geometries through novel representations and custom laser exposure strategies.

Image above – Fine struts in additively manufactured lattices are best built with custom exposure strategies for better mechanical performance and faster build times.

Lattice manufacturing

Manufacturing of fine details requires precise control of the laser energy, as the melting on each layer of the lattice build often comprises thousands of sparsely distributed exposures. There currently is at least one system that features a modulated laser focused down to 70 microns spot size, enabling production of struts and walls as thin as 140 microns.

Image above – A volume of 8,000 cubic cm of architectured material made from Ti6Al4V.

Future challenges

For all their attractions, there remain some barriers to deploying lattices in production parts. A key challenge is to substantiate the suitability of the design for stressed applications, particularly where fatigue is the critical performance attribute. By necessity, lattices contain lots of ‘as built’ surfaces and sharp intersections, which create stress raisers. To balance this out, lattices have a lot of built-in redundancy, and so may not fail catastrophically.

These characteristics make structural parts with load-bearing lattices best suited to applications where the loads are either constant or single, dynamic events. Cyclical load bearing applications look likely to be a little further off.

A related concern is how to validate lattice quality in manufacturing. The complexity and inaccessibility of lattice features makes them hard to inspect. CT scanning offers a solution, albeit a somewhat time-consuming one. The best answer here is likely to be in-process monitoring, so that we can demonstrate that each element of the lattice material has been built correctly.

Summary

Complex lattice structures can deliver exceptional product performance – both in efficiency and functional terms. They are key tools in component light-weighting, and can also boost heat transfer, energy absorption, insulation and joining performance. Careful lattice design can introduce precisely tailored properties into efficient components.

Additive manufacturing is often the only practical way to produce such intricate materials. A great amount of detail needs to be invested in investigating the latest software tools and selection of an AM machine that is optimized for fine detail work.

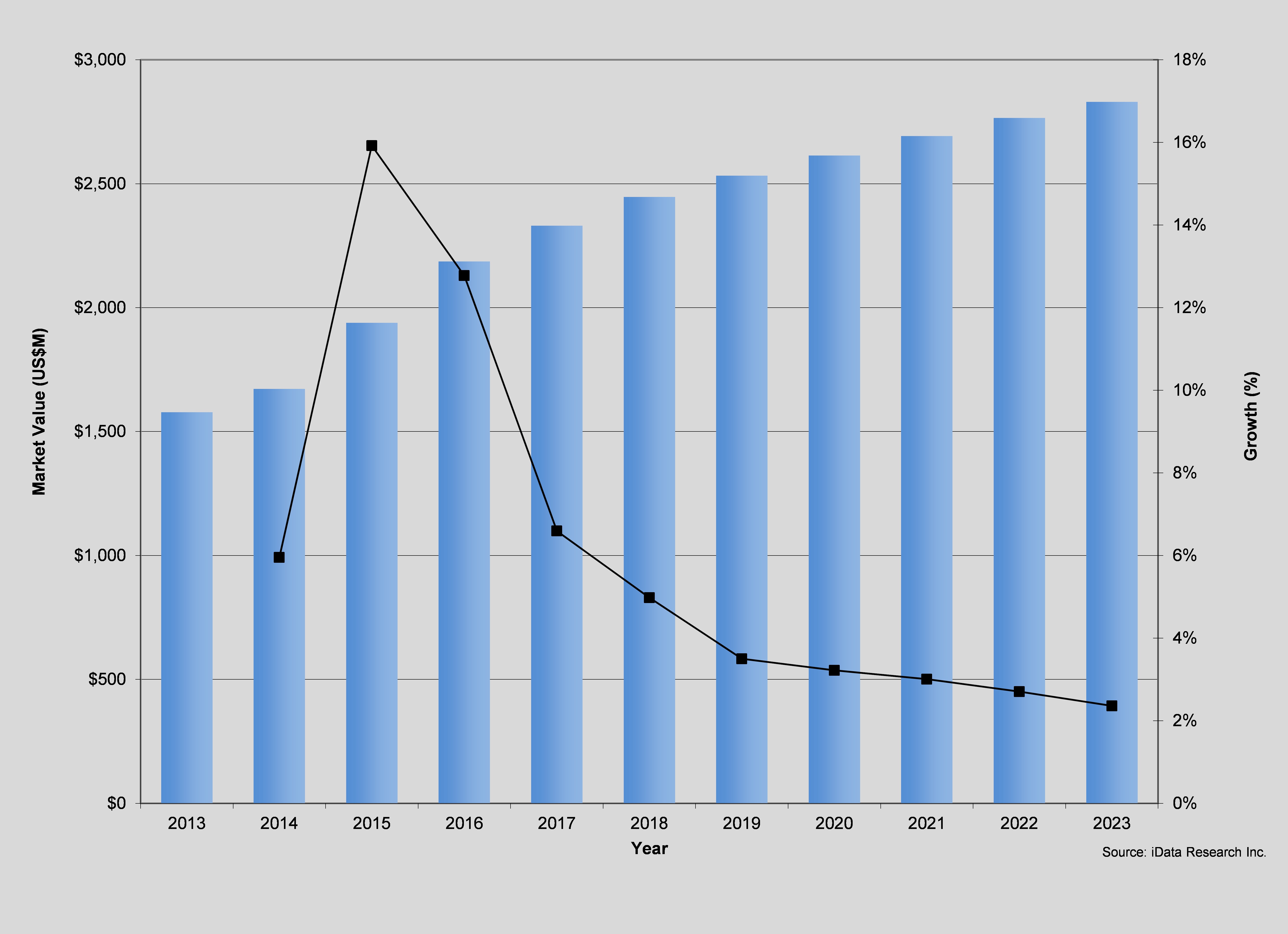

The market growth of minimally invasive device segments is expected to outpace that of traditional segments. MIS approaches such as lateral lumbar (LLIF) and oblique lumbar (OLIF) interbody fusion are expected to increase their procedure volumes significantly. However, decreasing pricing will somewhat offset the growth seen in market value. Growth of the total minimally invasive device market is expected to slow down over the coming years as the market stabilizes. Overall, the patient base will continue to grow driven by key demographic trends, which in turn strongly incentivizes hospitals and manufacturers alike to develop and update their product lines.

The market growth of minimally invasive device segments is expected to outpace that of traditional segments. MIS approaches such as lateral lumbar (LLIF) and oblique lumbar (OLIF) interbody fusion are expected to increase their procedure volumes significantly. However, decreasing pricing will somewhat offset the growth seen in market value. Growth of the total minimally invasive device market is expected to slow down over the coming years as the market stabilizes. Overall, the patient base will continue to grow driven by key demographic trends, which in turn strongly incentivizes hospitals and manufacturers alike to develop and update their product lines. Minimally invasive technologies are also expected to play an increasing role in spine procedures in the United States. In particular, lateral and oblique approaches (LLIF and OLIF, respectively) have generated growing interest and use by hospitals. Thus, LLIF and OLIF procedure volumes are projected to outpace both standard procedures and minimally invasive PLIF and TLIF counterparts in their cumulative average growth rate for the forecast period ending in 2023.

Minimally invasive technologies are also expected to play an increasing role in spine procedures in the United States. In particular, lateral and oblique approaches (LLIF and OLIF, respectively) have generated growing interest and use by hospitals. Thus, LLIF and OLIF procedure volumes are projected to outpace both standard procedures and minimally invasive PLIF and TLIF counterparts in their cumulative average growth rate for the forecast period ending in 2023.